Investors Should Look at Private Equity for Returns

In today’s prolonged low-yield environment, it is very challenging for investors and their advisers to identify opportunities that will enhance portfolio returns. As we look into the future, the solution may not come from public equities or other traditional investments. The public equity markets have been strong performers during the past few years, making up for years of poor performance during the great recession. But when equities run out of steam, where do investors turn for solid returns?

Well-informed advisers know they need to be looking at investments that provide both current yield and “alpha.” The use of alternative assets such as real estate, natural resources, and hedge funds is established and growing, and more recently individual investors have received entrée to private equity through new structures that now provide access to this largely institutional asset class.

Private equity investing may broadly be defined as investing in the securities of privately held businesses through a negotiated process. Private equity investment strategies are typically a transformational, value-added, and active investment strategy. It calls for a specialized skill set which is a key due diligence area for investors’ assessment of a manager.

Private equity represents a significant component of the alternative investment universe and is broadly accepted as an established and important asset class within many institutional portfolios. Today, many advisers are getting access to this coveted asset class through private offerings and more broadly through public vehicles such as non-traded business development companies.

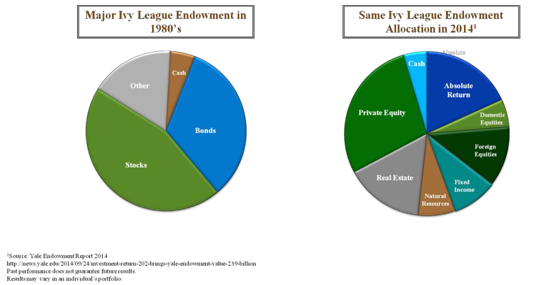

The primary reason so many institutional investors such as Yale’s endowment have emphasized private equity as a core element of their portfolio allocation strategy is to improve the risk and return characteristics of their overall portfolio. Investing in private equity offers investors the prospect to generate higher absolute returns while improving portfolio diversification and reducing overall volatility.

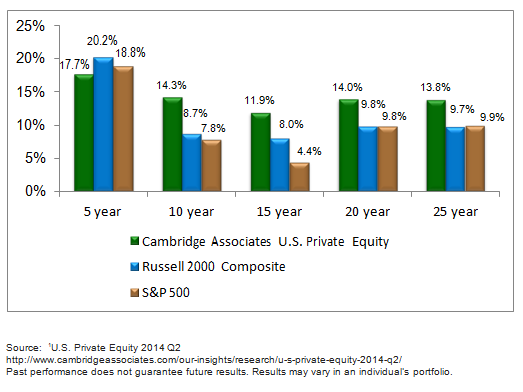

Track Record of Private Equity

The Private Equity Growth Capital Council (PEGCC) reported that as of June 30, 2014, returns from private equity funds (net of fees) beat the S&P 500 (including dividends) for a 10-year period by 6.5 percentage points per year. Returns to U.S. public pension funds from their private equity investments for the 10-year period also beat the S&P 500 by 5.9%, PEGCC research shows. This return premium can make a huge difference when compounded over a multi-year period. For many institutions, such a premium over more conventional asset classes justifies the different risk profile of the asset class, including its lack of liquidity.

Private equity as an asset class has been no stranger to institutional investors like endowments, pensions and institutions. While a typical U.S. public pension plan allocates around 9% of its assets to private equity, other groups – like endowments might allocate considerably more. Yale’s endowment, considered to be one of the top performing endowments, allocates about 33% to private equity.

One reason private equity traditionally outperforms public markets is the greater depth of information available to private equity managers. This helps managers more accurately evaluate a company’s proposed growth plan and to project performance. This greater access to information contributes significantly to reducing risk in private equity investments. Equivalent information in the public markets could be considered “inside information”. For most retail investors, accessing private equity funds is largely unattainable. The principal reason why individual investors have not historically invested in private equity funds is the high entry barriers. For example, minimum investment thresholds for many private equity fund has been $10 million or more and is usually only available to Qualified Purchasers.

Finally, even if those criteria are met, access to private equity has traditionally taken the form of a closed-end limited partnership, a generally unfamiliar opaque structure to an investor used to mutual funds.

Evolution is Afoot

Private equity managers have been exploring ways to democratize and bring private equity to a broader retail audience. Once such company is Triton Pacific, which has been a private equity fund manager since 2001. To reach a broader audience, Triton Pacific recently launched a publicly registered non- traded business development company, Triton Pacific Investment Corporation, which is available to both accredited as well as non-accredited investors. This is just another step in the right direction of making private equity funds available to individual investors.

When looking at constructing an investment portfolio, investors should always consider their overall goals and how to best meet those needs. As an asset class, private equity can offer significant potential for capital appreciation, adding to the ‘alpha’ portion of an investor’s portfolio.