Opening Salvo in the Longevity Annuity Revolution – QLACs

Good news about both aging and taxes! Thanks to an action taken by the IRS, there is good news that will save retirees money and help to better secure his or her income in later years.

On July 1, 2014, the Internal Revenue Service and the Treasury Department released final regulations on the treatment of qualifying longevity annuity contracts, or QLAC’s. These final regulations provide an exception to the required minimum distribution (RMD) rules of Internal Revenue Code Section 401(a)(9).

The IRS recognizes the risk that millions of Boomers may outlive their retirement assets and if they don’t plan properly, will be left living on Social Security and a small pension, if they are lucky. We believe that QLACs will lead the way to frank discussions about how these and other longevity annuities will revolutionize retirement income planning.

This exception allows individuals to exclude up to the lesser of 25% of account balances of certain qualified plans (defined contribution, 401(k), 403(b), 457(b)) and IRA’s, or $125,000, from the computation of RMD. To qualify for this reduction in RMD, the individual must purchase a deferred income annuity (DIA) that qualifies as a QLAC.

QLACs – A New Type of Annuity

To qualify, the DIA must meet certain requirements, such as no cash value, no surrender withdrawal or commutation features.

Thus, the insurance companies must manufacture a product that is low cost without certain features people know to seek in an annuity contract. The Journal of Accountancy goes as far as stating that the new regulations create “a new type of annuity.”

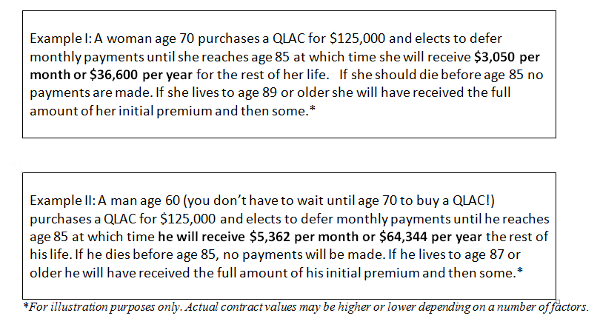

QLAC Examples

The QLAC specifies payments are to begin at a specific age, no later than age 85. These payments will last for the individual’s life. Prior to these regulations, all DIA’s in qualified accounts would be subject to RMD at age 70 ½.

As shown in the examples below, a relatively small premium paid today will generate not only years of tax benefits, but a strong stream of insured future income.

Note that in both examples, the purchasers chose a signal life annuity. This choice gives you the largest payment per month. The IRS does allow QLACs to offer death benefits in the form of joint and survivor annuities and return of premium (ROP) options. In Example II, if the purchaser had opted for an ROP, his monthly benefit would be $3,457 or $41,484 per year.

RMD Reduction

By excluding the value of QLAC’s from the account balances used to compute RMD, an individual can increase his or her tax-deferral by delaying QLAC payments up until age 85. If an individual maximizes a QLAC purchase of $125,000 by age 70 ½, and starts receiving payments at age 85, he or she would defer over $90,000 in income.

Think of this: A deferral of over $90,000!

Conclusion

QLACs will provide flexibility in retirement income planning and will help protect the individual from outliving his or her savings. This is a tremendous opportunity. Many retirees complain about their RMD and do not really need the money. Worse, their RMD may push them into a higher tax bracket, trigger taxes on their Social Security, and increase their Medicare costs.